[ad_1]

FOMC Rate Decision, Nasdaq 100, VIX, US Dollar and EURUSD Talking Points:

- The Market Perspective: USDJPY Bullish Above 132.00

- The FOMC rate decision ended as expected with a 25bp hike to a range of 4.50-4.75 percent, but the reiterated warnings of further hikes ahead didn’t sway the markets

- A Dollar tumble seems caught up in rate cut speculation and the drop in the VIX, but uneven fundamentals raise questions on the trend and an ECB decision makes EURUSD a high risk

Recommended by John Kicklighter

Get Your Free Top Trading Opportunities Forecast

Speculative traders in the broader markets seem to be satisfied in their collective forecast. Despite some highlights of an unflattering economic outlook and of course the FOMC’s commitment to fulfilling the rate hike stretch it began in 2022, the ‘risk oriented’ side of the market climbed after the event while the Dollar suffered a notable drop. It is not unusual for the markets to deviate on outlook from officials, but there is generally a risk in fostering this disparity from underlying fundamental course. And, the further the stretch on speculative exposure against these unfavorable circumstances; the worse the eventual fallout can be when the resolution comes to pass. In the meantime, a look at the markets in the aftermath of the Fed. The Nasdaq 100 arguably had the most pressing technical picture with the recent break above the 200-day simple moving average (SMA). The 2.2 percent rally with a three week high volume is impressive. Further, the ratio of the Nasdaq 100 to the Dow Jones Industrial Average (‘growth’ relative to ‘value’) rose to its highest level in three months suggesting a particular appetite for ‘riskier’ assets.

Chart of Nasdaq 100 Futures with 200-day SMA, Volume and 1-Day ROC (Daily)

Chart Created on Tradingview Platform

What was the motivation for the charge in risk assets and the further slump in perceived fear via measures like the VIX volatility index? Clearly, the run took place after the announcement of the FOMC rate decision. However, the outcome of that event doesn’t offer much in the way of genuine support for those plotting a long-term bullish market. The 25bp rate hike in the benchmark range to 4.50 to 4.75 percent is the highest among its major peers, but it was nevertheless fully priced in and thereby a minor factor. The real impact came from the elements used to project what happens from here. In the policy statement, the Fed kept in language suggesting a few more rate hikes was likely. Fed Chairman reiterated that perspective in his Q&A period. That isn’t exactly a surprise given what the central bank had projected in its SEP released with the December meeting – they projected a terminal rate of 5.1 percent (or 5.125 average) – but the markets have maintained skepticism that they will follow through. Furthermore, the Fed’s believe that it would not hike this year was repeated without changing the market’s disbelief.

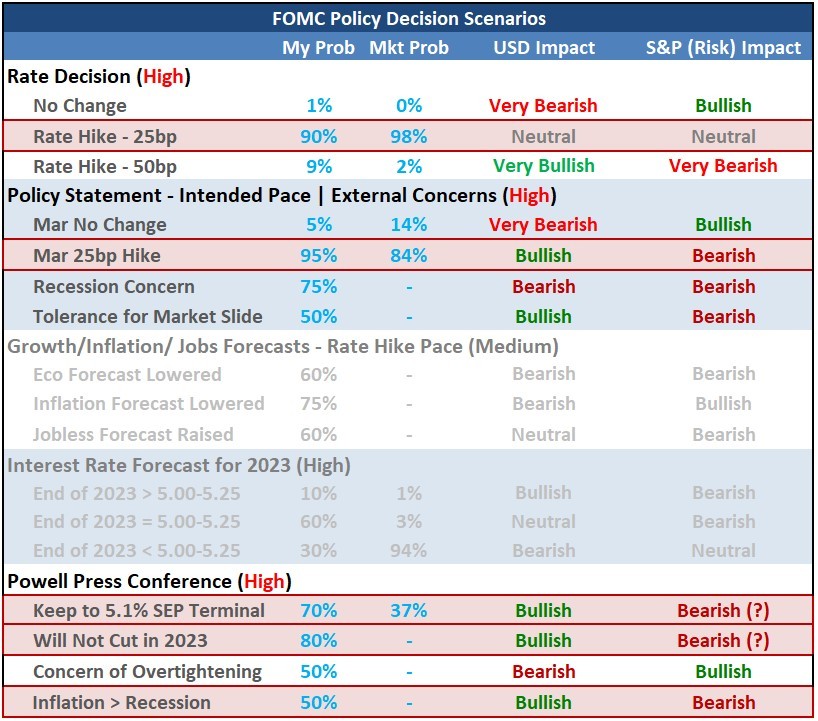

FOMC Scenario Table with Highlighted Outcomes

Table Created by John Kicklighter

By most accounts, the Fed’s policy decision was a mildly hawkish outcome; but overlaying the market’s skepticism, it comes off as a step away from a peak rate and eventual cuts. Whether the market’s divergent view on policy course is founded in the inflation forecast or perhaps the unrelenting association of a dovish Fed that capitulates at the sign of trouble from the past decade, the bulls have their guiding light. While I maintain a healthy skepticism over central bank commitments based on forecasts which necessarily have to change, it seems unlikely that the Fed will deviate from its inflation fight. If they are forced from that path, it would likely come in response to a particular troubling recession picture or financial crisis – both of which are greater threats to risk trends than easier monetary policy is a boon. Nevertheless, the market can operate on its own views until there is something hard and fast to dissuade the house view. Another market that finds itself in an impressive position is the US Dollar. The DXY Index dropped to its lowest level since April after dropping through the midpoint of the 2021-2022 range. While the US sports a higher yield and market-forecasted terminal rate than most of its counterparts, the Greenback’s backing as a safe haven seems to pulling it down (with the drop in VIX) and the speculation of Fed hikes in the second half (which may also be suppressing the VIX) is posing direct pressure.

Chart DXY Dollar Index Overlaid with VIX Volatility Index and Implied Fed Change in 2H (Daily)

Chart Created on Tradingview Platform

As we move into the back half of the week, I will be keeping a vigilant eye on the lift behind the renewed ‘risk appetite’. Just because I’m dubious of the foundation of a charge, doesn’t mean that the markets will have to rebalance to that outlook. As the saying goes ‘markets can remain irrational longer than you can solvent’. Then again, high profile event risk can generate serious circumspection on unevenly held believes. Looking at the docket for the next 48 hours, there will be a lot of challenge to fundamental stability. The ECB and BOE rate decisions will offer a bigger picture of monetary policy in context of risk taking. After Meta’s charge afterhours Wednesday, we will have the run of Amazon, Google and Apple after close Thursday. Then on Friday, we have the US nonfarm payrolls.

Top Global Macro Economic Event Risk for Next Week

Calendar Created by John Kicklighter

For a top market on my ‘must watch’ list, the EURUSD is easily the most interesting. It is the largest component of the DYX Index, so there is much of the same impressive technical performance on display. For this benchmark cross, the 1.2 percent charge was the biggest since November 11th – when the pair made its definitive turn after the US CPI release. What’s more, the charge pushed the exchange rate above the midpoint of its January 2021 to September 2022 bear wave. That said, the fundamental weight is serious here. This is the most liquid currency cross, so the Dollar’s have status is dampened here. That puts greater scrutiny on the relative interest rate standing, and the ECB is seen capping its own rate hike cycle well below the Fed. Will that factor in?

Chart of EURUSD with 20-Day SMA and 1-Day Rate of Change (Daily)

Chart Created on Tradingview Platform

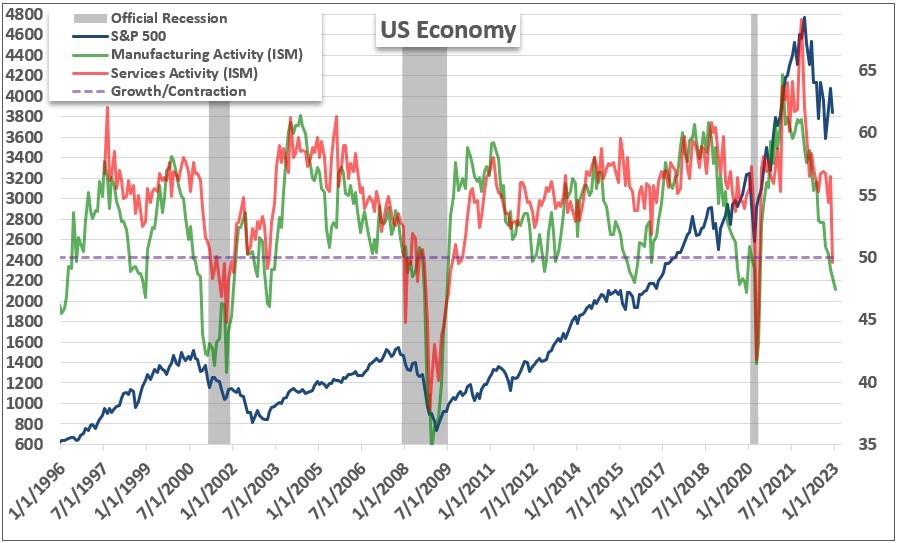

While there is a lot of event risk on tap and plenty capable of generating discrete volatility, the most interesting event through week’s end in my book is the ISM service sector activity report. Overlooked this past session was a deepening slide into contraction for manufacturing activity according to the same group. That does not bode well for a market that seems confident on the trajectory of growth. The US economy is heavily skewed in employment and output in services, so if last month’s surprise contraction is extended, it could break through the market’s complacency on risks ahead.

Chart of S&P 500 with US Mfg and Service Activity, Overlaid with Official Recessions (Monthly)

Chart Created by John Kicklighter

Discover what kind of forex trader you are

[ad_2]