US Dollar, USD, DXY Index, Fed, TIPS, Yields, ECB – Talking Points

- US Dollar resumed strengthening last week on Fed hawkishness

- The Fed reminded markets of their intention and yields responded

- If the northern winter is a harsh one, will EUR/USD resume its downtrend?

Recommended by Daniel McCarthy

Traits of Successful Traders

The US Dollar has started the week slightly firmer as the markets contemplate a Federal Reserve turning more hawkish at their March Federal Open Market Committee (FOMC) meeting in late March.

The possibility got legs after Cleveland Fed President Loretta Mester and St. Louis Fed President James Bullard made hawkish comments last week.

They both indicated that they would consider a 50 bp lift of the Fed funds target rate at the next meeting. While Ms Mester is on the board, she is currently a non-voting member.

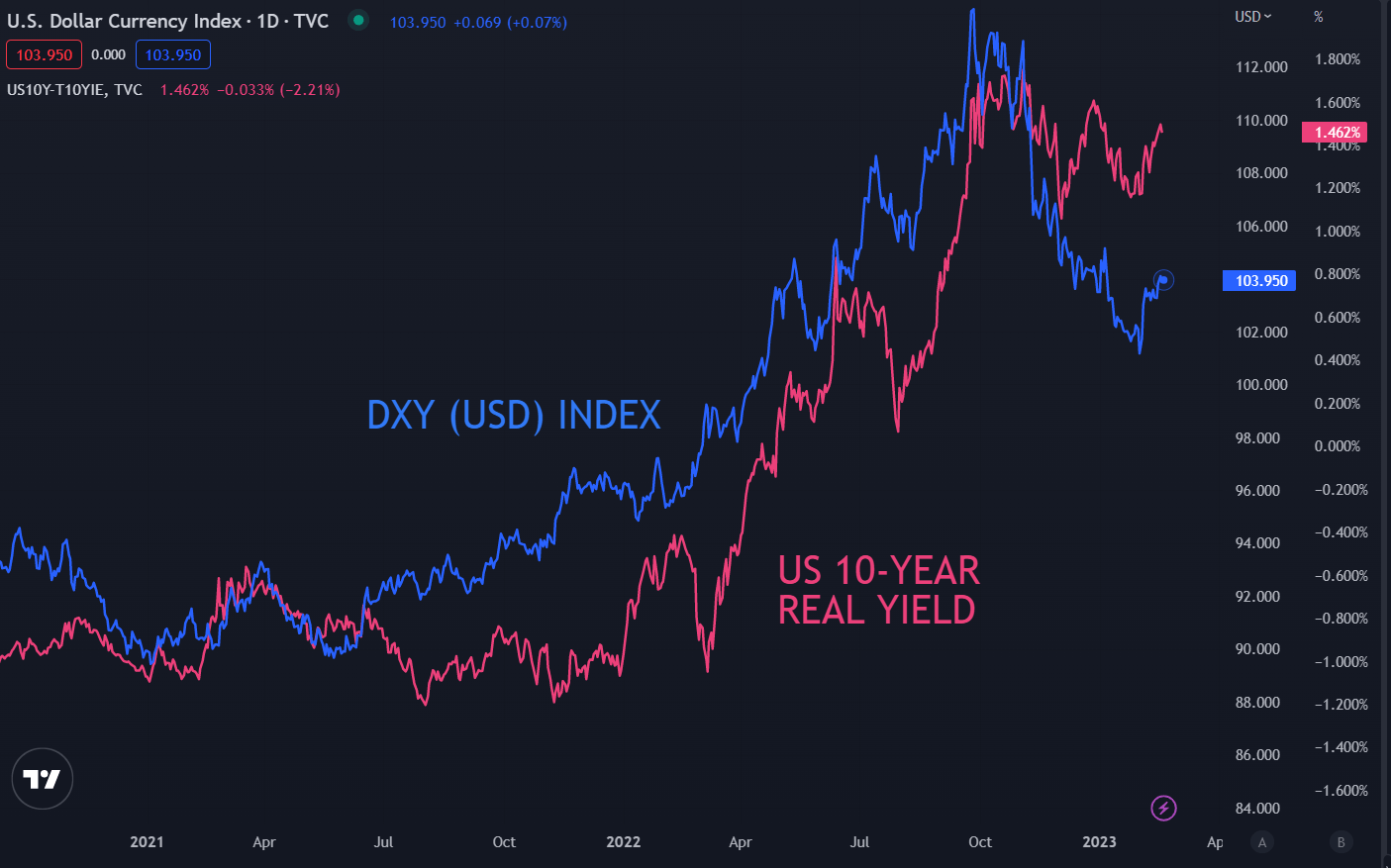

This saw Treasury yields move north into the end of last week and although the US bond market is closed today, the increase in real yields appears to be underpinning the US Dollar.

Real yields are the nominal Treasury yield minus the market-priced inflation rate derived from the Treasury Inflation Protected Security (TIPS) over the same period.

If the Fed decides to go with 50 bp moves, this would be a surprise to markets as the swaps and futures markets are both currently pricing in 25 bp at the next two FOMC gatherings.

The European Central Bank has indicated that they will be moving in 50 bp at their next meeting but their cash rate is more than 200 bp below the Fed.

Trade Smarter – Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

Subscribe to Newsletter

Geopolitical tensions in the APAC region continue with North Korea firing 2 missiles over the Japan Sea on the weekend. This was followed by the US and South Korea performing combined military exercises today and then 3 more missiles were fired by North Korea on Monday.

This comes on the back of simmering US-China relations after the balloon saga of last week. This has contributed toward a broader concern for risk assets although APAC equities were mixed today.

Australian and Japanese stock indices are fairly flat while China and Hong notched modest gains.

A notable underperformer today has been New Zealand’s S&P/NZX 50 Index which is down over 1%. The cost of cyclone Gabrielle and the prospect of the Reserve Bank of New Zealand (RBNZ) hiking by 50 bp to 4.75% on Wednesday appear to be dragging it lower.

Crude oil prices eked out small gains with the WTI futures contract is pressing toward US$ 77 bbl while the Brent contract is having a look above US$ 83.50 bbl. Gold is steady, trading near US$ 1,842 at the time of writing.

Looking ahead, it could be a quiet day with the US on holiday and aside from EU consumer confidence, there is little in the way of data.

Later in the week, FOMC meeting minutes will be released on Wednesday and the Fed’s preferred inflation gauge of Core PCE will be out on Thursday as well as some 4Q US GDP figures.

The full economic calendar can be viewed here.

{{GUIDE|HOW_TO_TRADE_}}

DXY (USD) INDEX AGAINST US 10-YEAR REAL YIELD

— Written by Daniel McCarthy, Strategist for DailyFX.com

Please contact Daniel via @DanMcCathyFX on Twitter