[ad_1]

EQUITY MARKET OUTLOOK:

- The S&P 500 and Nasdaq 100 trade modestly lower in the wake of the U.S. inflation and retail sales report

- The recent jump in Treasury yields is a headwind for stocks, but the reduced probability of a hard landing should cap any downside

- This article looks at key Nasdaq 100 technical levels to watch in the coming sessions

Recommended by Diego Colman

Get Your Free Equities Forecast

Most Read: USD/JPY Pushing Higher on US Dollar Strength and Yen Weakness

US equities staged a strong rally at the beginning of the year, but have lacked a strong directional bias of late. True, we have had some positive sessions this month, but we have also seen several negative days, with the net effect of little upside or downside moves, as the tug-of-war between buyers and sellers remains contested and unresolved. Against this backdrop, both the S&P 500 and Nasdaq 100 are virtually unchanged since Monday of last week, despite elevated volatility, but intraday both benchmarks are posting modest losses.

The latest U.S. inflation report, released on Tuesday, did little to provide clarity for investors, but may be quietly raising risks to the equity market. For context, January headline CPI came in at 6.4% year-on-year, two tenths of a percent above expectations, a sign that inflationary the process of restoring price stability will be long and bumpy.

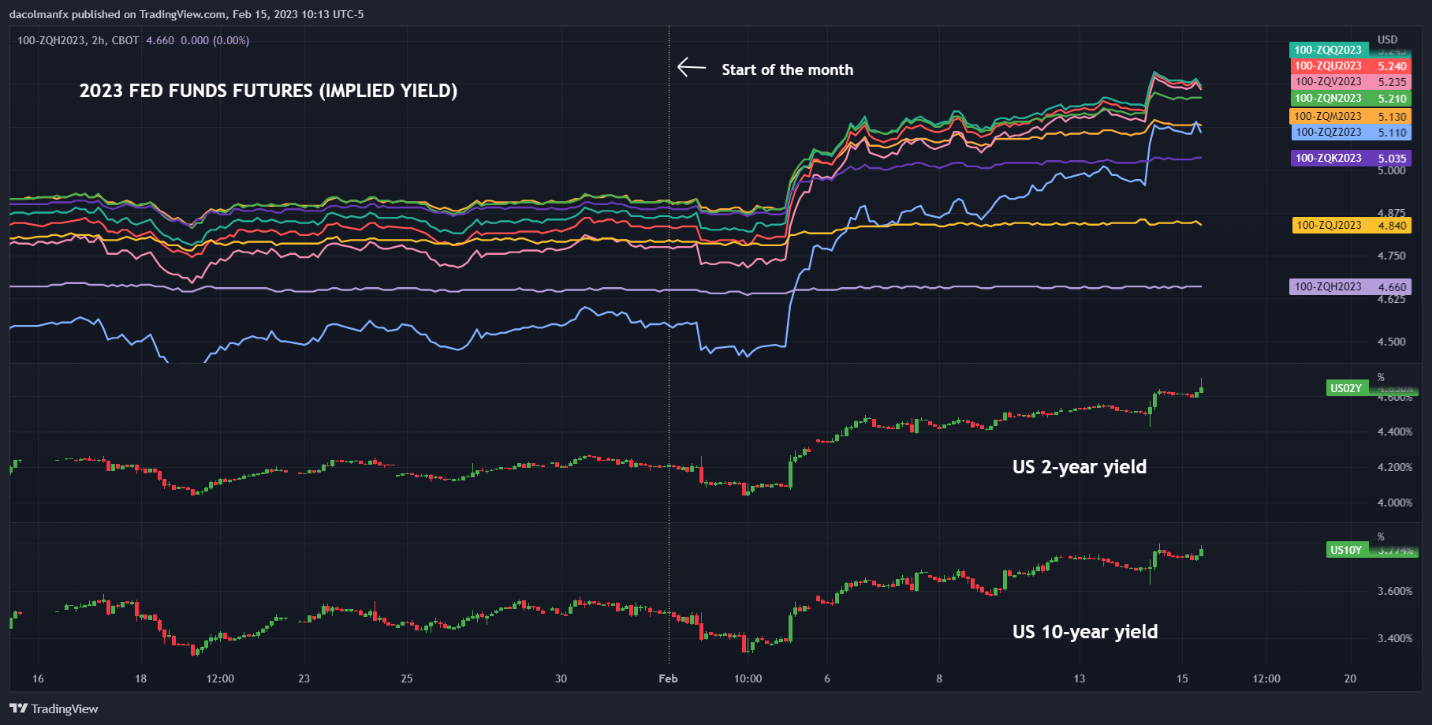

Sticky inflationary pressures have bolstered U.S. Treasury yields across the curve, particularly those on the short end as investors start to fully embrace the view that the Federal Reserve’s terminal rate will have to settle higher than initially anticipated. This dynamic can be appreciated in the chart below which shows borrowing costs peaking at 5.245% (implied yield for the August Fed funds futures contract).

FED FUNDS FUTURES & TREASURY YIELDS

Source: TradingView

If there was any doubt about the need for a more restrictive monetary policy stance over the forecast horizon, today’s solid macro data may have helped to dispel some of the deep misgivings. According to the U.S. Department of Commerce, advanced retail sales surged 3% m-o-m in January, the largest increase in nearly two years. This is a clear indication that household spending remains robust despite the central bank’s forceful tightening campaign to slow demand.

With tight labor markets, elevated wage pressures and resilient consumer spending, the stars may be aligning for more FOMC hikes and higher-for-longer interest rates. This scenario may depress sentiment and create headwinds for stocks, especially those in the technology sector. However, the reduced likelihood of a hard landing will prevent a major bleeding for now, caping selloffs on Wall Street.

All of this leaves us with the question: when might U.S. stocks begin to rebound in a sustainable way? The answer is not simple, but one thing is clear: the road ahead will be bumpy. Until corporate earnings bottom out and begin to show tentative signs of recovery, investors will be reluctant to deploy significant capital in equities. Against this backdrop, it is difficult to be extremely optimistic about the S&P 500 and Nasdaq 100 prospects in the short term.

Recommended by Diego Colman

Improve your trading with IG Client Sentiment Data

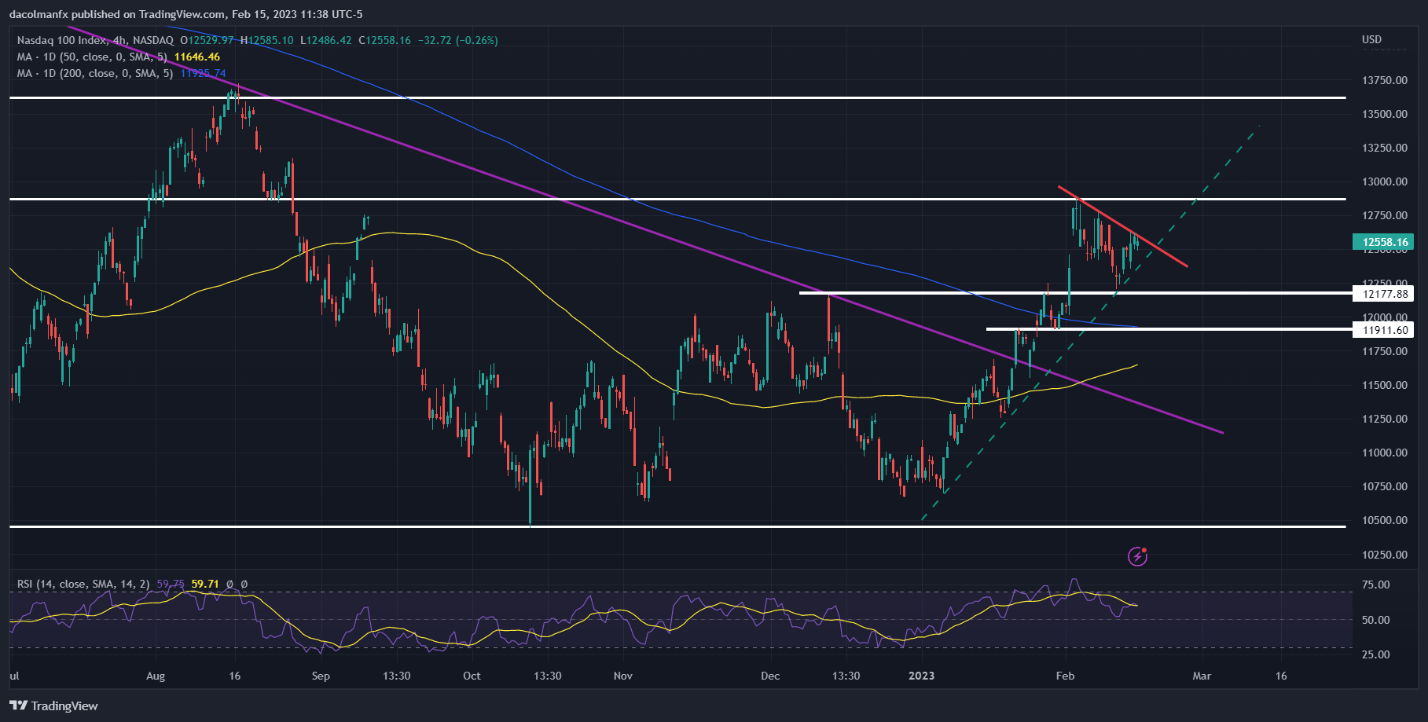

NASDAQ 100 TECHNICAL ANALYSIS

After conquering multi-month highs in early February, the Nasdaq 100 has been inching lower, guided by a short-term descending trendline extended off the recent peak. If selling momentum accelerates, the tech index may find support at 12,400, but if this area is breached on the downside, we could see a move towards 12,200, followed by 11,900. On the flip side, if buyers return to the market and trigger an upswing for stocks, initial resistance appears at 12,625. On further strength, the focus shifts to 12,870, the 38.2% Fibonacci retracement of the 2021-2022 sell-off.

NASDAQ 100 TECHNICAL CHART

[ad_2]