[ad_1]

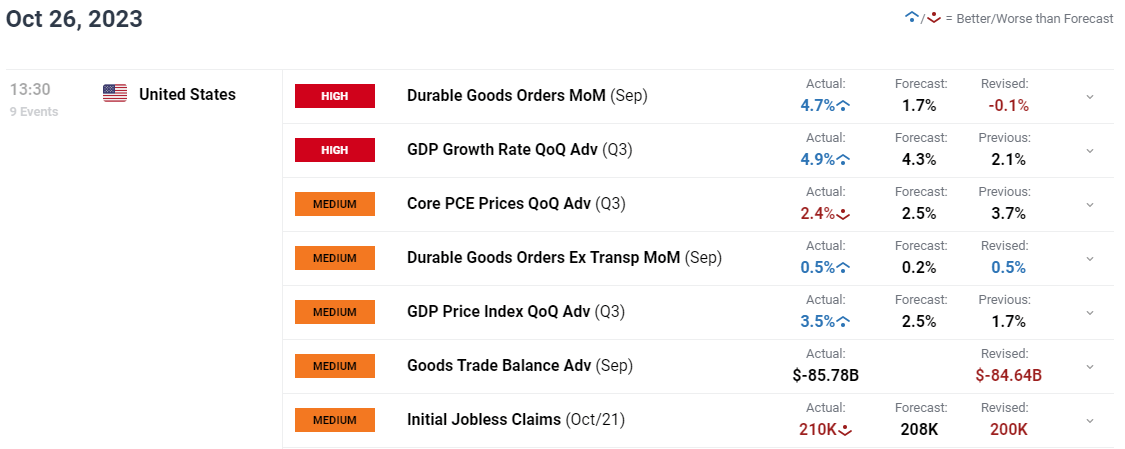

US GDP Q3 ’23 (PRELIM) KEY POINTS:

READ MORE: S&P500, NAS100 Weighed Down by Tech Earnings and Rising Yields. 4000 Level Up Next?

Recommended by Zain Vawda

Get Your Free USD Forecast

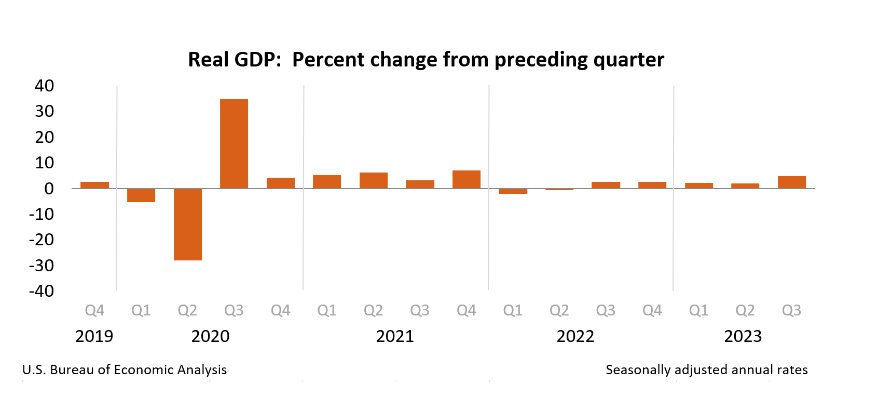

Real gross domestic product (GDP) increased at an annual rate of 4.9 percent in the third quarter of 2023, this according to an advanced estimate by the Bureau of Economic Analysis. This is the most since the last quarter of 2021, above market forecasts of 4.3% and the previous print of a 2.1% expansion in Q2.

Customize and filter live economic data via our DailyFX economic calendar

Consumer spending rose 4%, the most since Q4 2021 (vs 0.8% in Q2 2023), led by consumption of housing and utilities, health care, financial services and insurance, food services and accommodations and nondurable goods (led by prescription drugs) as well as recreational goods and vehicles. Exports soared 6.2%, rebounding from a 9.3% fall in Q2 and imports also increased (5.7% vs -7.6%). Private inventories added 1.32 pp to growth, the first gain in three quarters. Most interestingly however, residential investment rose for the first time in nearly two years (3.9% vs -2.2%) this despite the extremely high mortgage rates in the US.

Source: US Bureau of Economic Analysis

Personal saving was $776.9 billion in the third quarter, compared with $1.04 trillion in the second quarter. The personal saving rate—personal saving as a percentage of disposable personal income—was 3.8 percent in the third quarter, compared with 5.2 percent in the second quarter. This has been a figure i have been watching closely as if this continues then the US economy could come under strain in Q4 or Q1 of 2024 as consumers continue to deplete their savings to keep up with cost-of-living increases.

US DURABLE GOOD ORDERS

New orders for manufactured durable goods in the US surged by 4.7% month-over-month in September 2023, rebounding from a 0.1% contraction in August and significantly surpassing market expectations of a 1.7% rise. This is the largest increase in 3 years and was primarily driven by strong demand for transportation equipment.

US ECONOMY MOVING FORWARD

The US economy has continued to surprise and remain resilient in the face of many challenges. The Fed according to many are ‘winging’ with policymakers themselves admitting that these are unprecedented times. The rest of the quarter is unlikely to offer any kind of reprieve as there are still a host of risks for the US economy and US Dollar to navigate.

The First will be averting a government shutdown before November 17 which should come to fruition following the election of a new House Speaker in Republican Mike Johnson. A Government shutdown could be detrimental to US growth prospects for Q4. October is also the first month that student loan payments resumed since October 2020. I have spoken about this at length over the past couple of months and it appears to already be having an impact. According to recent data 37% of households are struggling to pay expenses up from 32% in September.

Source: Apollo, The Kobeissi Letter

In stark contrast however the US home sales data yesterday showed a surge in September as homebuilders appear to be taking on some of the cost of higher mortgages with new homes a better option for buyers at this stage.

The funadamentals may be a bit mixed but on the rate front the USD is in the driving seat and likely to remain supported. The technicals may show the USD to be in overbought territory with a small technical inspired retracement a possibility but unlikely to be sustainable. The potential for safe-haven demand through Q4 continues to grow as well which makes the US Dollar an intriguing prospect heading toward the end of the year.

Recommended by Zain Vawda

How to Trade Gold

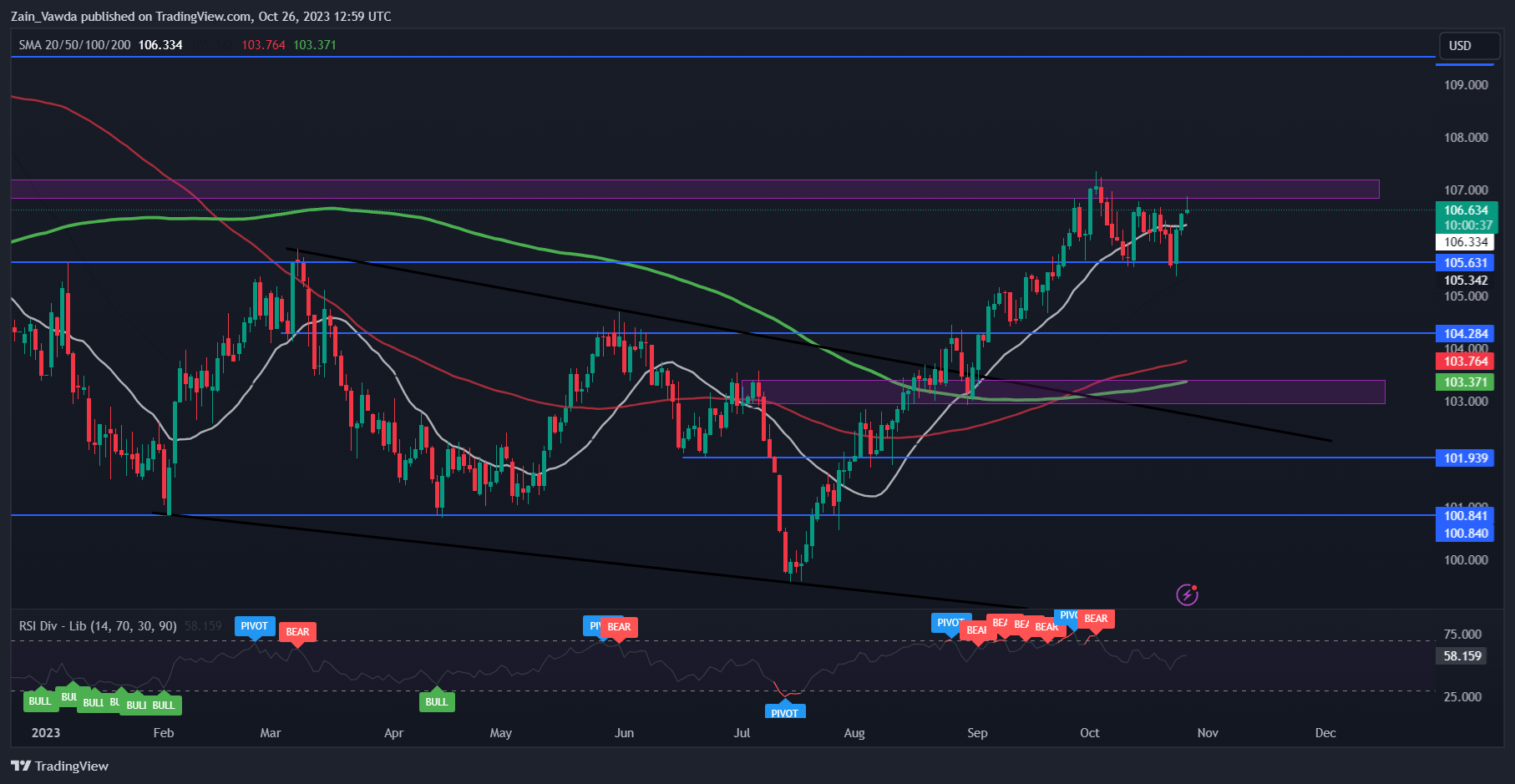

MARKET REACTION

The initial market reaction was relatively subdued with the DXY turning cautious at a key area of resistance around 106.80-107.20. This area will be key for USD bulls if we are to see the DXY rally continue. Right now, it’s a tough one to call as the fundamental factors support the US Dollar whereas the Technicals hint an imminent retracement.

DXY Daily Chart, October 26, 2023

Source: TradingView, prepared by Zain Vawda

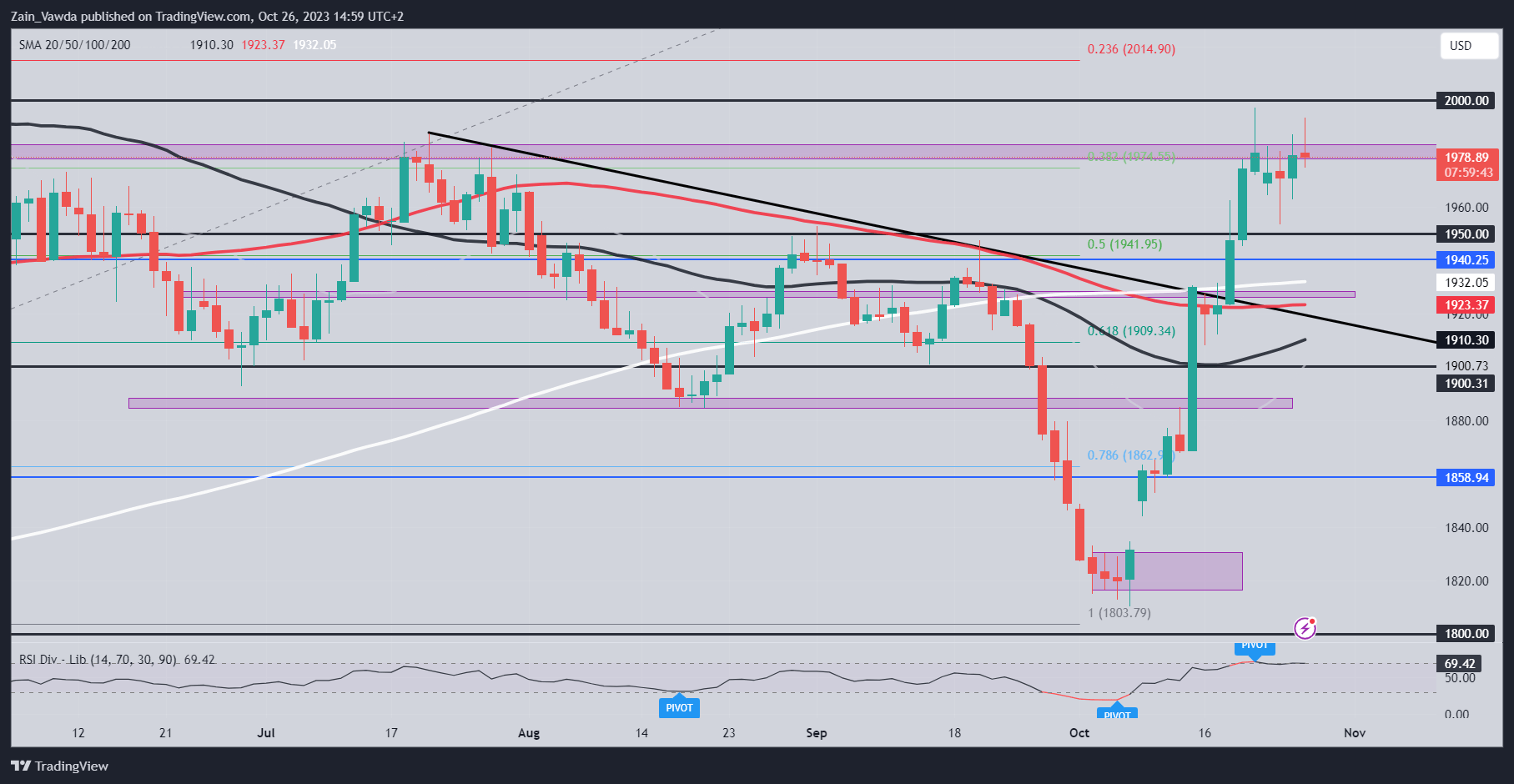

GOLD REACTION

Gold did experience a bit of a pullback following the news release, but safe haven appeal continues to underpin the precious metal. Right now, for a sustained retracement lower only a change in the overall risk sentiment in regard to Geopolitical risks can likely lead to a sustained selloff in Gold. Central Bank meetings next week are likely to be important but could also be overshadowed by the risk profile of markets heading into the meetings.

XAU/USD Daily Chart, October 26, 2023

Source: TradingView, prepared by Zain Vawda

IG CLIENT SENTIMENT

Taking a quick look at the IG Client Sentiment, Retail Traders have maintained a more bullish stance of late with 61% of retail traders now holding long positions. Given the Contrarian View to Crowd Sentiment Adopted Here at DailyFX, is this a sign that Gold may begin to fall?

| Change in | Longs | Shorts | OI |

| Daily | 2% | -6% | -1% |

| Weekly | -17% | 19% | -6% |

— Written by Zain Vawda for DailyFX.com

Contact and follow Zain on Twitter: @zvawda

[ad_2]